Principles for Founder Equity Allocation: How to Get It Right?

Thinking through how to split equity among co-founders.

Splitting equity among founders is one of the earliest and most consequential decisions you’ll make. It doesn’t just shape who owns what - it forces you as a newly formed founding team to really get a common understanding and alignment about what fairness and ownership means at a deep level. Yet despite its importance, it often feels like a taboo topic. Or worse, it’s reasoned by analogy: "We’ll just split equally. That’s what everyone does."

When I was in the process of finding the right co-founders (a journey I reflected on here), I knew eventually we’d approach this question. And I didn’t want to rely on analogies or precedent: I wanted to understand what was actually fair and right in our specific context. That meant digging deeper, asking better questions, and thinking this through from first principles.

The more I spoke to other founders and investors, the more I realised how wide the spectrum of opinions really is. One view that stuck with me: “An equal split makes no sense. It’s impossible that everyone contributes exactly the same over the entire lifetime of a company.” Therefore, the first principle at work here was: if you had perfect information about the future and you could put a value on the contribution to the respective value creation over the lifetime of the company, you would be in a position to allocate the equity optimally. As one obviously cannot predict the future, it got me thinking, what does it actually mean to contribute to value creation? What are the proxies of value creation that a founding team brings over the lifetime of a company?

Discussing what everyone brings to the table

Out of that exploration emerged a pattern that helped me structure the conversation. Not as a rigid formula, but as a way to surface what each person brings to the table across five key areas:

Skillset & experience

Uniqueness & replaceability

Contribution of assets

Roles & responsibilities

Founder mindset, risk, and commitment

I’m sharing this not as the answer, but as a starting point. My goal is to help other early-stage founders reflect more deeply before making this important decision. Because when done thoughtfully, equity allocation becomes more than a spreadsheet exercise: it becomes a foundation for fairness, ownership, and long-term alignment; and most importantly - for really important conversations upfront.

Let’s look at each of the categories.

1. Skillset & Experience

Starting with the obvious: what skills does each founder bring to the table, and how relevant are they to the company at which stage? In our case (building in health tech), expertise in product, data & engineering, marketing, fundraising and clinical work all mattered, but not equally at every moment. You need to weigh not just what someone can do, but how crucial that is at which stage of the company. I would slightly overweight the early stage skills because it is the phase you are the least likely to get past.

At the same time if you have really key scaling skills and you eventually make it past the first product market fit, it is a huge asset. As a result, beyond domain knowledge, leadership experience also matters eventually. Has this person built and scaled teams before? Can they attract top talent? Have they shown they can thrive in ambiguity and push through the chaos that defines the early days? Most importantly - are they despite that still hands-on and the right fit for the first phase?

2. Uniqueness & Replaceability

Next is a harder, more uncomfortable question: how easily could this person be replaced? It’s about scarcity. Does this person bring a set of perspectives, skills, or credibility that’s hard to find elsewhere? That might be deep insight into an underserved user group, or a rare blend of technical and operational experience. Uniqueness earns weight because it changes what the team can build thanks to this person.

3. Contribution of Assets

Not all contributions are time or skills. Some founders bring critical assets to the table: access to capital, investor relationships, proprietary IP or frameworks, or a strong network of future talent or potential customers. In early-stage companies, these can materially shift the odds of success. For example, a founder who’s built deep trust with great early stage investors, or who has unique insight into the problem at the forefront of science or technology adds disproportionate value (especially before product-market fit).

4. Roles & Responsibilities

What will each person actually own? Clarity on roles helps prevent friction down the road, but it also helps quantify what’s on the line for each founder. As part of the “co-founder dating questionnaire” you discuss which founder will own which areas of the business. I would suggest using that as a guide here.

Some roles come with visible pressure and public-facing scrutiny. Others are more behind-the-scenes but just as foundational. You want to map this clearly before you try to weigh the contribution.

There is also a reality that once you reach Series A or B stage, the accountability of the CEO towards investors and the broader public is an additional weight that needs to be factored in. Investors at later stages also expect a clear ultimate tiebreaker in decision making.

5. Founder Mindset, Risk & Commitment

Finally, and maybe most importantly: where is each person coming from, and what are they putting on the line? Is this a side project or a mission? Did they join early, when it was mostly risk and vision, or later, when momentum had started to build? Are they willing to sacrifice salary, take real financial risk, and commit for the long-term?

You could get even more “scientific” with modelling the opportunity cost between the founder salary and the market salary they are foregoing by starting this company as opposed to whatever else they would pursue. Perhaps this is very different between co-founders and hence needs to be reflected more strongly. I would advise not to get overly scientific here, though and ensure that directionally it feels fair.

This last piece might not show up on a resume, but it shows up over time. You want to build with people who’d keep going in the hardest of times, people who are in it because they believe in what you’re building and why it matters.

Aligning on principles before percentages

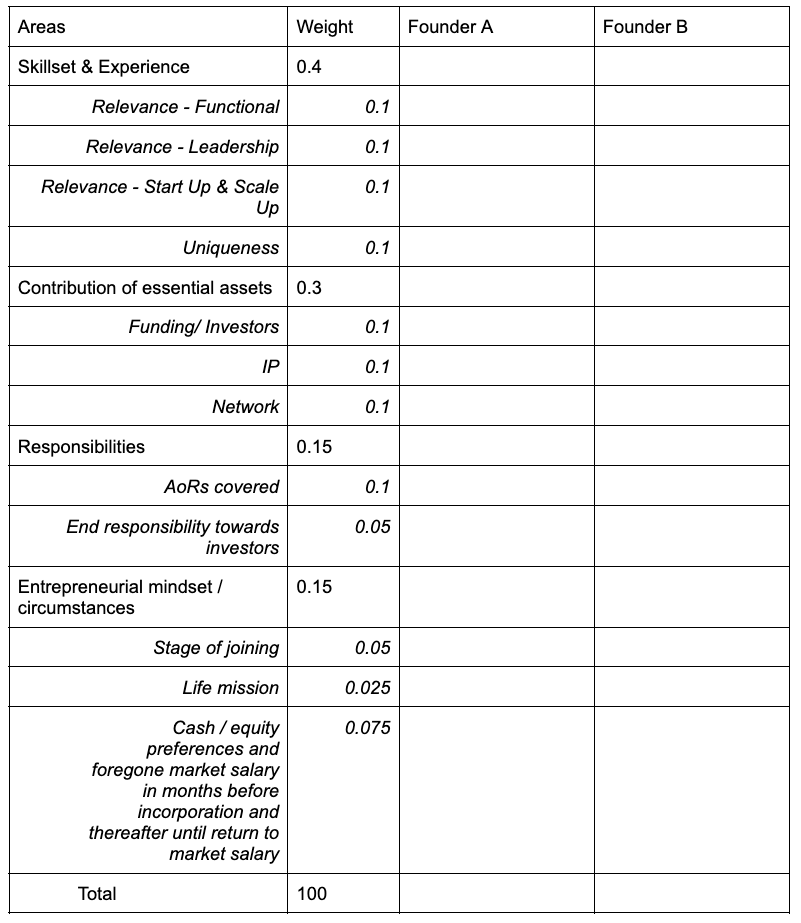

When it came to navigating the equity split, I didn’t want to start with percentages, I wanted to start with aligning on how we make this decision. Rather than “assessing” one another, I drafted a framework outlining the dimensions I believed mattered and my proposed weighting of each factor, but left the actual values blank.

Taking that extra step changed everything. What followed wasn’t a negotiation in the traditional sense: it was a principle based conversation. We discussed what fairness looks like in our specific context, what each of us brings to the table, and how we want to handle future decisions. The process itself became a reflection of the company we’re trying to build. Here below you can find the template including the weighting we landed on in the hope it is helpful and gives you a sense of the first principles at play here. The weighting will be different in your situation, as will be some of the nuances of what you factor in. However, I wanted to share this, to bring the above to life.

Ultimately, this only works if you’re willing to accept the outcome of doing it collaboratively. If you agree on the categories and weightings and after that set the actual numeric values together, you have to walk the talk even if the numbers are different than what you perhaps had wanted them to be before the conversation.

Of course, not every founding team needs this level of nuance. If you’re a group of uni friends starting something fresh, the split might naturally be equal. But when you’re a complementary team with 10–25 years of experience across software, medicine, and business (and with different entry points to the journey) then the discussion becomes more nuanced. Just splitting it equally without thinking this through would have the potential to bring about a feeling of unfairness and resentment.

Lastly, I would always advise to rather err on the generous side. A few percentages up or down are not worth anything if the team does not feel full ownership and a fair distribution. Remember, in the end, this process isn’t only about who gets what. It is about setting the tone for how we work together. And that might be the most valuable outcome of all. I hope you find this helpful and look forward to any comments!